benefitsCompensationCompensation & Benefitscompensation strategycompensation surveyspay-scalestrategyWhy Having a Compensation Strategy is a Must April 21, 2024February 4, 2015 by Liz Maier-Liu How much should you pay your employees? Why should you have a compensation strategy? And when…4 minute readRead More

CompensationCompensation & BenefitsIncentivePayPay Allocationvariable pay4 Compensation Topics You Can’t Afford to Overlook April 21, 2024January 21, 2015 by Liz Maier-Liu When the word "compensation" is brought up in conversation, most people assume it just refers to…3 minute readRead More

CalendarCompensation & BenefitsPayPay PeriodsWorkplace Policies & PracticesPay Period Leap Year: Handling 27 Pay Periods August 11, 2023January 13, 2015 by Liz Maier-Liu If the question of, “How will you handle 27 pay periods,” doesn’t sound familiar to you,…4 minute readRead More

CompensationCompensation & BenefitsInformation TechnologyITsalaryIs IT Salary Growth Keeping Pace with Job Demand? August 11, 2023November 6, 2014 by Liz Maier-Liu With much discussion in 2014 over what city will be the next Silicon Valley, it seems…4 minute readRead More

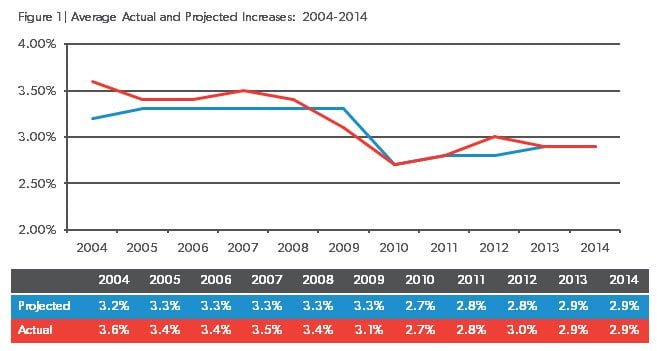

CompensationCompensation & BenefitsRaisesRaises Remain Steady Among Northeast Ohio Employers August 11, 2023September 18, 2014 by Liz Maier-Liu Post-Recession Pay Adjustments are Stable With raises over the few years to 2014 holding steady at…3 minute readRead More

benefitsCompensationCompensation & BenefitsExecutivePayPerks5 Key Types of Executive Compensation August 11, 2023June 11, 2014 by Liz Maier-Liu Executive compensation plans come in a wide variety of shapes and sizes depending on what business…3 minute readRead More

CompensationCompensation & BenefitsIncentivesMost Employers Offer Pay Incentives, Shift Focus to Short-Term August 11, 2023June 4, 2014 by Liz Maier-Liu In May of 2014, pay incentives, primarily at the uppermost executive levels, have been seeing quite…3 minute readRead More

CompensationCompensation & Benefitssalary4 Tips for Reading and Analyzing Salary Ranges August 11, 2023May 14, 2014 by Liz Maier-Liu A key aspect of any healthy compensation plan is transparency. Due to the potentially charged nature of…3 minute readRead More

CompensationCompensation & BenefitsmedianCompensation Planning Tips: What is the Median? August 11, 2023May 14, 2014 by Liz Maier-Liu When it comes to compensation planning, one of the most important figures to have on hand…4 minute readRead More

CareWorksCompensation & BenefitsManaged Care OrganizationMCOChoosing an MCO (Managed Care Organization) August 11, 2023April 29, 2014 by Liz Maier-Liu ERC is proud to endorse CareWorks as the preferred workers’ compensation Managed Care Organization for its'…2 minute readRead More

401kCompensation & BenefitsretirementHelping Employees with Retirement Transition August 11, 2023April 1, 2014 by Liz Maier-Liu People can feel overwhelmed when it comes to transitioning to retirement. Many just don’t know how…5 minute readRead More

401kCompensation & BenefitsOswald FinancialretirementIs Your Company on the Right Track with 401(k) Plans? March 30, 2014 by Liz Maier-Liu http://www.yourerc.com/cost-savings/retirement-plan-services Dave Kulchar talks about Oswald Financial's unique PlanSuccess 401(k) Behavioral Audit program. This tool…5 minute readRead More